In-depth report on the beer industry: From the rise of craft beer to see the upgrade of beer consumption

2016/02/20

.jpg")

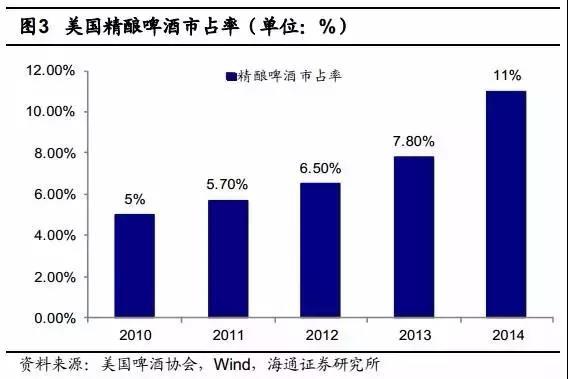

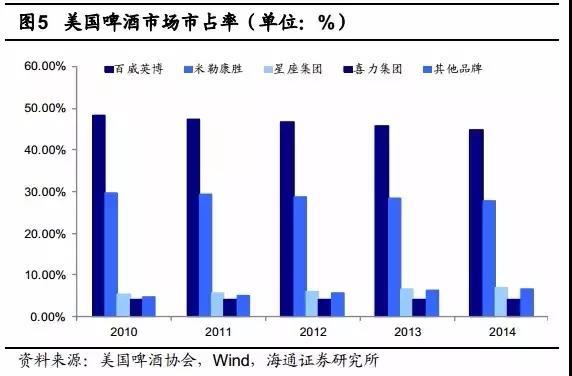

The rapid rise of craft beer in the United States has accounted for 20% of the market share. Craft beer has boomed in the United States over the past five years. In 2014, the sales volume of craft beer in the United States was 2.664 million tons, a year-on-year increase of 18%, and the sales volume was 19.6 billion US dollars, a year-on-year increase of 22%. The market share was 11% in terms of sales volume and 19% in terms of sales. In stark contrast to this, the overall beer market in the United States is increasingly sluggish. In 2014, the total sales volume of beer only increased by 0.47%, and the CARG in the past five years was -0.30%. In 2014, the CR3 of the American beer market was 80%, which was 3.5 percentage points lower than that in 2010, reflecting the fierce competition faced by traditional beer companies from craft beer.

Craft beer is coming in menacingly, big companies deal with mergers and acquisitions。Large beer companies generally enter the craft beer market by establishing independent subsidiaries or acquiring craft breweries. In the 1990s, major beer companies in the United States began to try to build their own craft breweries, but the results were not satisfactory. In recent years, in addition to self-built craft breweries, major American beer companies have begun to acquire craft breweries on a large scale, and then use their own channels for sales. Among the major beer companies in China, Zhujiang Beer took the lead in producing craft beer.

The combined profitability of craft beer products and traditional large company channels is expected to increase significantly.Whether it is Anheuser-Busch InBev, SABMiller or other beer companies, the impact of the craft breweries acquired at this stage on their financial statements is not obvious, but their amazing growth rate and effective supplement to the existing product line make them The big beer companies couldn't give up. Judging from the continuous merger and acquisition cases in recent years, these giants are undoubtedly full of expectations for the future of craft beer. Anheuser-Busch InBev and others wantonly acquired craft breweries and used their own channel advantages to sell craft beer products. This strategy can not only quickly promote its craft beer, but also directly increase the company's net profit margin in the future.

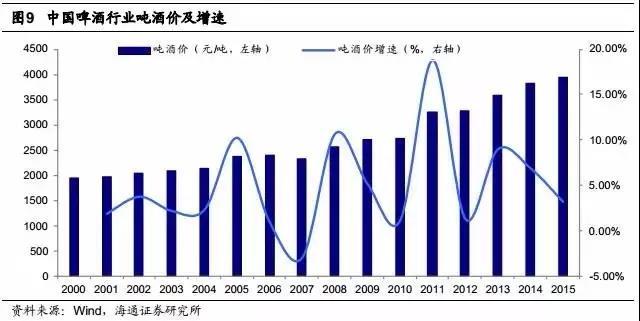

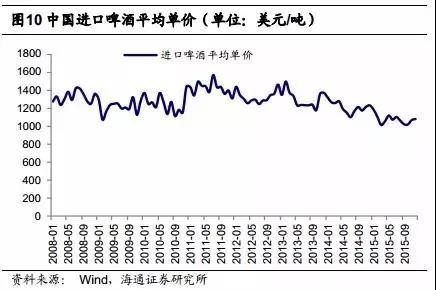

Domestic beer has missed the golden decade of consumption, while imported beer is an episode and craft beer is the trend.From 2000 to 2015, the total retail sales of domestic social consumer goods increased by 6.7 times, while the sales of beer increased by 3.3 times over the same period, and the price of beer per ton of wine increased by less than 1 times. The decline in the average price of imported beer and the increase in the average price of domestic beer companies indicate that Chinese consumers are becoming more rational about imported beer, and domestic beer companies are also changing their business strategies and focusing on product upgrades. It will take time for domestic beer giants to get involved in craft beer on a large scale, but the advantages of craft beer and the characteristics of domestic beer consumption channels may make craft beer an important direction for product structure upgrading.

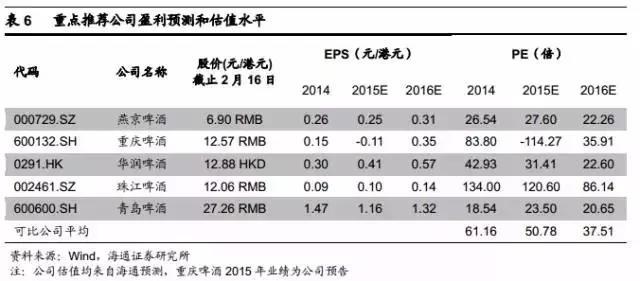

Give the industry an "overweight" rating.According to Wen Hongwei's research team, the profitability of the beer industry will undergo an inflection point change.The main reasons are: first, beer consumption has entered a mature stage, and it is out of date for leading companies to compete for shares at low prices, and it will become a trend to shift from "seeking share" to "seeking profits"; second, the CR5 of the beer industry is close to 80%, and the competition pattern is initially stable; third, Due to reasons such as equity incentives and shareholder replacement, most listed beer companies have increased their motivation to improve their performance. Based on this, the beer sector as a whole will usher in investment opportunities. Prioritize Zhujiang Beer, which is the first to focus on craft brewing, Chongqing Beer, which has significantly improved its main business, and China Resources Beer, which has a large potential for net profit growth. At the same time, it recommends obvious regional advantages and state-owned enterprise reforms Expected Yanjing Beer and Tsingtao Beer.

1. Craft beer originated in the United States and flourished

Craft beer (Craft Beer) first originated in the United States. The three major characteristics of American craft beer are small scale, high autonomy and strong tradition. According to the accurate definition of craft beer by the Brewers Association, small-scale means that the annual output does not exceed 6 million barrels (the American beer barrel is about 120 liters), and the sales market share is less than 3%; autonomy It means that no more than 25% of the shares are controlled by large alcohol manufacturing companies; traditional restrictions limit the use of barley malt in craft beer due to cost reasons. Historically, the number of breweries in the United States has reached 4,131, most of which are breweries. In the 1970s, due to mutual mergers and economic downturn, there were less than 100 wineries left in the United States. Since the concept of craft beer became popular all over the world, in September 2015, the number of breweries in the United States once again exceeded 4,000, of which more than 3,400 were craft breweries.

1.1 There are significant differences between craft beer and traditional industrial beer

The two major categories of beer are Ale and Lager. Most craft beers belong to the category of ale beer, while industrial beer is generally lager beer. However, you cannot simply use Al and Lager to distinguish whether it is craft beer. Generally speaking, ale beer belongs to the top fermentation method, while lager beer is the bottom fermentation method. The top fermentation method usually ferments rapidly at a higher temperature (15-20 degrees Celsius), resulting in a richer body and a stronger fruit flavor. Due to the differences in craft beer brewing process, additives and selection of yeast, the taste of the brewed beer is very different, which is unmatched by mass-produced (Mass Product) industrial beer.

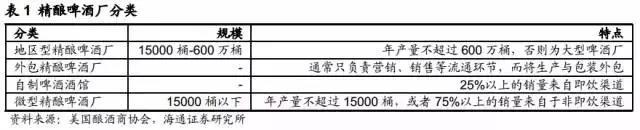

The American Brewers Association roughly divides craft breweries into four categories, regional craft breweries, outsourced craft breweries, self-made beer pubs and micro craft breweries.

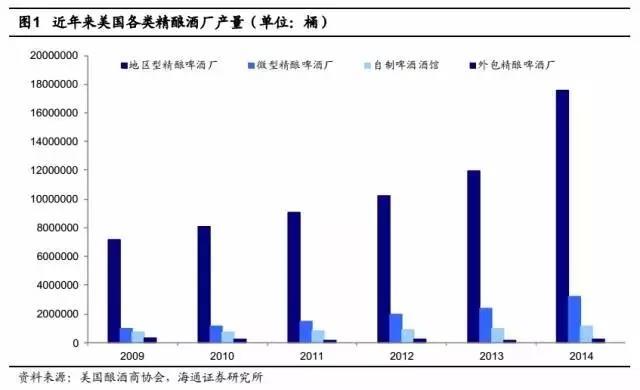

Most of the craft beer production in the United States comes from regional craft breweries and micro craft breweries. The proportion of outsourced craft breweries is shrinking, and homemade beer pubs are becoming more and more popular with consumers.

The unit price of American craft beer is significantly higher than that of the overall beer market. In 2014, the rising price of American craft beer was almost twice that of ordinary beer. Most American craft beers are mainly consumed by local people, highlighting the regional characteristics of the product. However, China's craft beer is still dominated by high-end consumers, concentrated in big cities such as Beijing, Shanghai, Guangzhou, Shenzhen, etc., highlighting the high specifications of the products. In addition, the price of ordinary beer in China is cheap, and the price of craft beer is about 4-5 times that of ordinary beer.

1.2 American craft beer accounted for nearly 20% and still grew rapidly

According to the American Brewers Association, in 2014, the United States produced about 2.664 million tons of craft beer, with a year-on-year increase of 18% in sales and 22% in sales, reaching US$19.6 billion. Sales accounted for 19.3% of the total beer market. The rate is 11%.

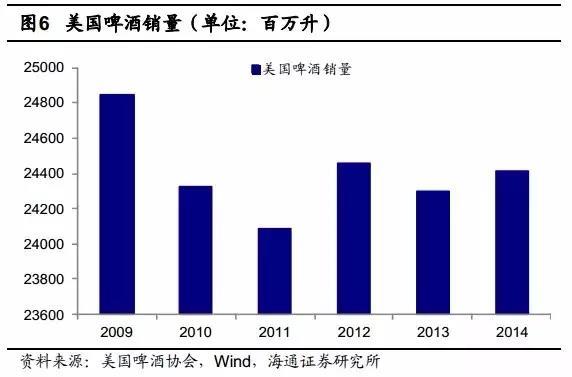

In the past five years, while craft beer has flourished, the overall beer market in the United States has been declining. In 2014, beer sales in the United States only increased by 0.47% year-on-year, and the CARG growth rate in the past five years was -0.30%. In 2014, the CR3 of the U.S. beer market was 80%, which was 3.5% lower than that in 2010, which also reflected the fierce competition from craft beer that big beer manufacturers faced.

The development of craft beer in the states of the United States also shows that the east and west coasts are significantly higher than those in the central part. In Vermont and Colorado, the per capita production was 16.2 and 13.6 gallons (US gallon is about 3.78 liters), respectively, while in Arkansas it was only 0.2 gallons.

2. Craft brewing is on the rise, and big companies are dealing with mergers and acquisitions

2.1 Beer giants first tasted "craft beer" through self-built

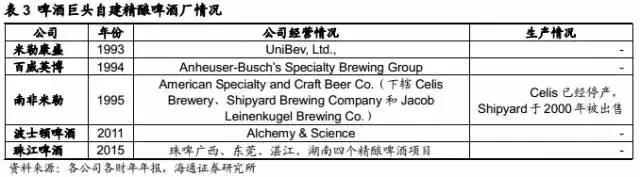

Generally speaking, big beer companies generally enter the craft beer market by establishing independent subsidiaries or acquiring craft breweries. As early as 1994, Anheuser-Busch’s Specialty Brewing Group was established by Anheuser-Busch InBev, dedicated to brewing handcrafted beer, which was the first for a large beer company to enter the craft beer market. In 1995, SABMiller founded American Specialty and Craft Beer Co., which has three brewing companies under its jurisdiction, but so far only Jacob Leinenkugel Brewing Co., which was purchased in 1988, remains.

In the 1990s, major international beer companies began to try to build their own craft breweries, but the results were not satisfactory. In July 2015, Zhujiang Beer was the first Chinese beer company to try to build its own craft beer production line.

2.2 Large-scale mergers and acquisitions, Budweiser Millers entered the craft beer market strongly

In recent years, in addition to building their own craft breweries, major beer companies have begun to aggressively acquire craft breweries and then use their own channels to sell them. This is also the most common way for foreign beer giants to operate craft beer. According to Dealogic statistics, in 2015 alone, 19 fine breweries in the United States were acquired or partially acquired, with a total transaction value of 13 billion US dollars. Due to the small size of craft breweries, Anheuser-Busch InBev has been ahead of major beer companies in large-scale mergers and acquisitions of craft breweries, and has continuously appeared in the headlines of mergers and acquisitions of various craft breweries.

Because the volume of craft beer is small and there are more craft breweries to choose from, it is expected that the mergers and acquisitions of major American beer companies will continue. Although the American Brewers Association has always been very cautious about the big beer companies, the major beer companies have been committed to gaining a share of the craft beer market and achieved good results. Nowadays, the craft beers under the big beer companies are usually not labeled with the name of the parent company, so that most consumers do not know that these craft beers come from big beer giants, such as Red Dog and IceHouse produced by SABMiller, which are marked as Plank Road Produced by Brewery, Goose Island, which originally produced craft beer, has been fully acquired by AB InBev. The Killian’s Irish Red craft beer produced by Miller Coorson even won the champion of the best-selling craft beer list of the year. The perfect system, advanced production equipment and channels all over the country of large companies make these craft beers have advantages that ordinary craft beer does not have.

In December 2012, the American Brewers Association published an article "Craft VS Crafty" (Craft refers to handicrafts, referring to craft breweries; while Crafty refers to the tricky behavior of big beer companies), suggesting that consumers be familiar with what they buy. products, and a special statement pointed out that the products produced by craft breweries acquired by large manufacturers will no longer be regarded as craft beer.

However, the cooperation between craft breweries and large companies is still going on vigorously. Many American craft brewery owners do not reject this form, and most consumers care about the quality of the products, not purely craft beer. Whether the beer comes from a traditional small brewery, the position of big beer companies in the field of craft beer in the future cannot be ignored.

3. Small and beautiful craft beer reports influence geometry

3.1 It is difficult to have a big impact on the reporting side in the short term if the proportion is low

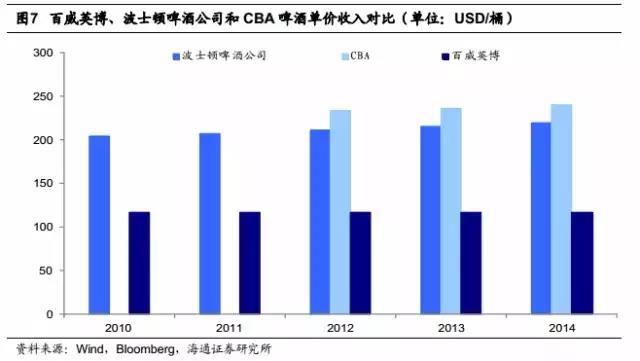

Whether it is Anheuser-Busch InBev, SABMiller or other beer companies, the impact of the craft breweries acquired at this stage on their financial statements is not obvious. Although the volume of craft beer is small now, its astonishing growth rate and effective supplement to the existing product line make big beer companies reluctant to abandon it. Anheuser-Busch InBev owns a 32% stake in the listed craft beer company Craft Brew Alliance (CBA). CBA’s operating income in 2014 was US$200 million. In 2014, Anheuser-Busch InBev’s (BUD) operating income was US$47.1 billion, and CBA accounted for a large proportion. Less than 0.5% (the CBA and BUD annual report deadlines are different, and the selected data are all the latest fiscal year data).

However, as the largest craft beer company in the United States, the size and strength of Boston Beer Company cannot be ignored by the big beer giants. The Boston Beer Company, founded in 1984, has achieved about 5% of Anheuser-Busch InBev's sales revenue, and in 2014 still achieved a year-on-year growth of nearly 22%.

3.2 Strategic complementarity is of great significance

Beer giants are not optimistic about the financial contribution of craft beer to the company at this stage, but judging from the continuous mergers and acquisitions in recent years, these giants are undoubtedly full of expectations for the future of craft beer. In addition, the income per barrel of craft breweries is significantly higher than that of AB InBev, but due to the scale, the gross profit rate and net profit rate lag far behind AB InBev. It is precisely because of this that Anheuser-Busch InBev aggressively acquired craft breweries and used its own channel advantages to sell craft beer products. This strategy can not only quickly promote its craft beer, but also directly increase the company’s net profit margin in the future.

By comparing Anheuser-Busch InBev with the two craft beer companies, the net profit margin of craft beer is significantly lower than that of AB InBev due to marketing expenses and other reasons. However, in the future, craft beer companies are expected to change the This status quo.

4. Domestic beer has missed the golden decade of consumption, imported beer is an episode, craft beer is the trend

4.1 The vicious competition between domestic beer has led to imported beer "taking advantage of the gap"

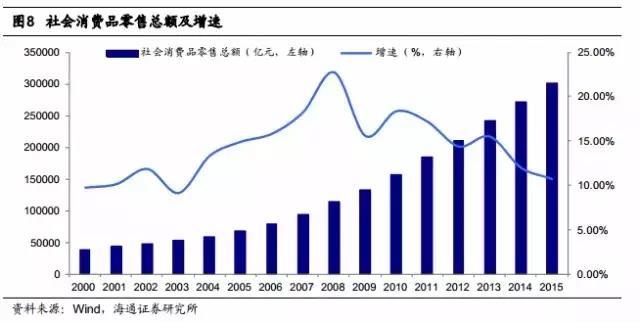

In the golden age of China's domestic consumption, the total retail sales of social consumer goods increased from 3.9 trillion yuan in 2000 to 30.1 trillion yuan in 2015, an increase of 6.7 times, while the sales of the beer industry increased by 3.3 times over the same period, and the price of beer per ton of wine increased by the same amount. to 1x.

In recent years, the number and variety of domestic imported beer have increased sharply. We believe that Chinese consumers favor imported beer mainly because of its "newness, novelty and specialness". "Sneaking in while taking advantage of the void" has seized the share of China's high-end beer market. However, unlike the dairy products that have been involved in product safety scandals and the wide variety of imported wines that are difficult to distinguish between good and bad, several major domestic beer companies have been cultivating in the Chinese market for many years, with relatively stable consumer groups and few safety problems. The requirement for freshness is high, and the long-distance transportation of imported beer will inevitably affect the taste, so the advantages of domestic beer companies are very obvious.

In particular, judging from the changes in the average unit price of overseas imported beer and the per-ton price of domestic beer companies in recent years, Chinese consumers are becoming more rational in the face of imported beer, and the unit price of imports is constantly falling, while the per-ton price of domestic beer companies is constantly increasing. Domestic beer companies are also gradually changing their business strategies, focusing on improving product quality and seizing the high-end market. In recent years, new domestic beer products such as Yanjing White Beer, Snowflake Pure Draft Series, Heavy Beer Fortress, etc., have been making continuous efforts to seize the high-end market and achieved good results.

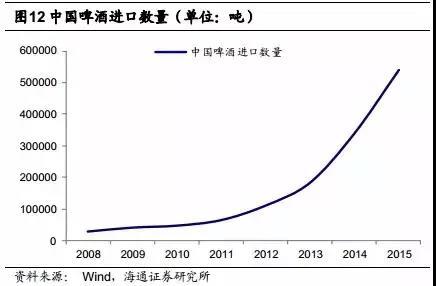

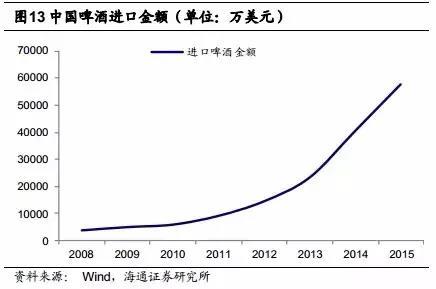

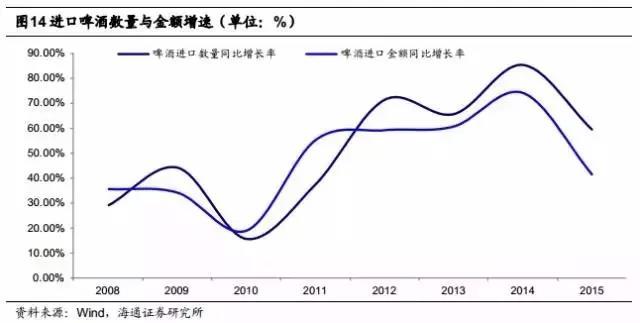

Judging from the quantity and amount of imported beer, the high-end beer consumption market is still advancing rapidly. In 2008, my country imported 28,100 tons of beer with a total value of 37.12 million US dollars. By 2015, my country imported 538,300 tons of beer with a total value of 575 million US dollars. However, in terms of growth rate, both the quantity and value of imported beer in China have begun to slow down. It is expected that as consumption tends to be more rational in the future, the advantages of imported beer will further decrease.

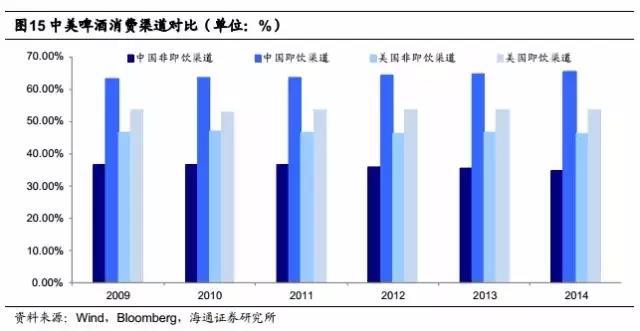

From the perspective of China's beer consumption channels (according to the amount), the main channels come from ready-to-drink consumption, such as restaurants and bars. In China, more than 60% of beer consumption is completed in ready-to-drink channels, while in the United States it is only slightly more than 50%. Since the consumer price sensitivity of ready-to-drink channels is lower than that of non-ready-to-drink channels, this also brings more room for upgrading the product structure of China's beer consumption.

my country's high-end beer consumption capacity is very strong, and the trend of product upgrading will continue in the future. Ending the "blind worship" of overseas beer, in addition to the spontaneous product upgrades of domestic beer giants, craft beer may increase the consumption level of the entire industry.

4.2 China's fine brewing is coming, and Zhujiang Beer is the first to set sail

In China, craft beer started relatively late. In 2008, Master Gao Beer Factory was established, which is regarded as the first craft beer enterprise. After several years of development, craft beer houses began to appear in major cities in China, gradually introducing craft beer products with Chinese characteristics. At the beginning of 2013, Master Gao launched the first bottled craft beer in China, marking that craft beer has gradually embarked on the road of multi-channel promotion. At present, major wineries, such as Zhujiang Beer, China Resources Beer, Tsingtao Brewery, etc., are also actively developing craft beer business. The more famous craft breweries in China now include Panda Brew, Beijing A Taproom, Boxing Cat (Boxing Cat) and so on.

Compared with the price difference between American craft beer and ordinary beer which is about 2 times, the price difference between Chinese craft beer and ordinary beer reaches 4 to 5 times, mainly because the current Chinese craft beer market is still in short supply, and many overseas buyers Chinese people, high-end white-collar workers, etc., so craft beer consumers have strong spending power. Most of the channels for craft beer are bars, high-end restaurants and high-end supermarkets. Now China's craft beer market has just started, and the competition is not yet fierce. The gross profit rate and net profit rate can reach 50% and 30%, respectively, which greatly exceed the level of mature craft beer market. However, the competition in China's craft beer market is bound to become more intense in the future. The price increase and profit margin of craft beer will definitely decline significantly in the future, but the consumer group will also show a trend of expansion.

China's craft beer industry started relatively late, but China's beer giants are gradually getting involved in the craft beer business. If Tsingtao Brewery and China Resources Snowflake were just testing the water at the beginning, Zhujiang Brewery was the first in the leading industry to try the craft beer project and accelerate the upgrading of product structure. In July 2015, the company announced that the non-public offering project plans to raise no more than 4.8 billion yuan, of which more than 250 million yuan is planned to be invested in the construction of the craft beer project, including four sub-projects in Guangxi, Dongguan, Zhanjiang and Hunan. The construction and implementation of the company's main factory area. The new production line will be used to produce high value-added craft beer, including puree barrel beer, 5L or 1L canned beer. A total of 8,000 tons of new production capacity was added, accounting for 0.68% of the company's sales volume in 2014, and the estimated after-tax financial internal rate of return was 15.13%.

In the short term, it will take time for Chinese beer giants to get involved in craft beer on a large scale. It is too early to reflect the benefits of craft beer from the report side. However, the advantages of craft beer and the characteristics of Chinese beer consumption channels may enable Craft beer has become a "sharp weapon" to promote the upgrading of the industry's product structure.

5. Summary

Since Anheuser-Busch InBev and SABMiller issued a statement on October 13, 2015, stating that the boards of directors of the two parties had reached an agreement on the key issues in the proposal of Anheuser-Busch InBev to acquire SABMiller, we have continued to investigate and track the beer industry, and have released China Resources Beer, In-depth reports from five companies including Tsingtao Brewery, Yanjing Beer, Zhujiang Beer, and Chongqing Beer.

We believe that the profitability of the beer industry will experience an inflection point change. The main reasons are: first, beer consumption has entered a mature stage, and it is out of date for leading companies to compete for shares at low prices, and it will become a trend to shift from "seeking share" to "seeking profits"; second, the CR5 of the beer industry is close to 80%, and the competition pattern is initially stable; third, Due to reasons such as equity incentives and shareholder replacement, most listed beer companies have increased their motivation to improve their performance.

Other

No content yet!